Quick Idea: $LSBK

- Small regional bank just completed de-mutualization.

- Current price of $12.66 is 0.7x BV ($17.89/sh).

- $100M market cap, $75M in cash.

- Activist Joseph Stilwell filed 9.4% stake, accumulated around $12.10/sh.

- Stilwell has record of pushing for buybacks/mergers.

Lakeshore Bancorp just completed its second-step conversion, so is a nice, simple tiny bank trading at a discount to book value ($140M). The book is mostly cash ($75M) raised from the conversion. An activist fund that has made an entire career out of going activist on these types of banks has taken a 9.4% stake.

There are restrictions on buybacks and mergers post de-mutualization, so this won't resolve overnight. To be honest, I'm not sure what all the restrictions are. In a post on this situation, @InvestSpecial (great follow!) speculates buybacks are a year out, and merger not allowed for three years.

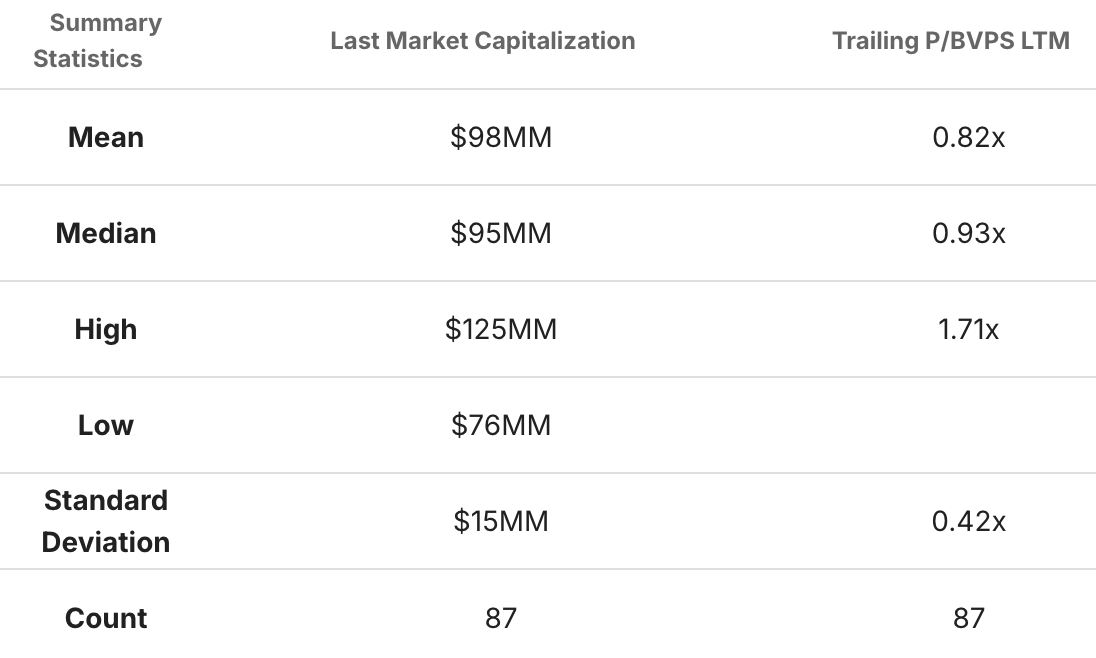

I was curious if the discount to book value was anything special. Pulling P/TBV for all US banks between $75M and $125M market cap on Tikr reveals that LSBK's ratio is a bit low, but not outrageously so. The standard deviation is also high.

A Boring Little Bank

The bank itself doesn't seem exceptional. Efficiency ratio last six months is 72% (expenses are 72% of net revenue) and RoE is 6%. The high efficiency ratio (typical bank is closer to 55%) probably means Stilwell can activist his way to some cost savings.

Seventy percent of LSBK's assets are loans. Ninety-five percent of the loans are real estate loans. Over half of those are commercial real estate. That's exciting. Provision for credit losses roughly 1% total, but provision for losses in the commercial loan portfolio at 1.3%.

Eighty-five percent of deposits are interest bearing. Loan-to-deposit ratio is 88%. Throw in the cash and securities and they could lose one third of deposits before having issues.

Not bad, not amazing. Let's call it a diamond-in-the-rough.

That's It

The bet is just that the bank trades up closer to book value, improves its cost structure, maybe builds a better loan book, initiates a buyback with some of its cash hoard eventually, and gets acquired a few years down the line. All of this is more likely to happen with the activist in the mix.

Risk is probably in the real estate concentration of the loan book, and just general timeline dragging out beyond three years. I think the risk of permanently losing money is low, but also its a small bank, so small position.

Member discussion